Share Price")

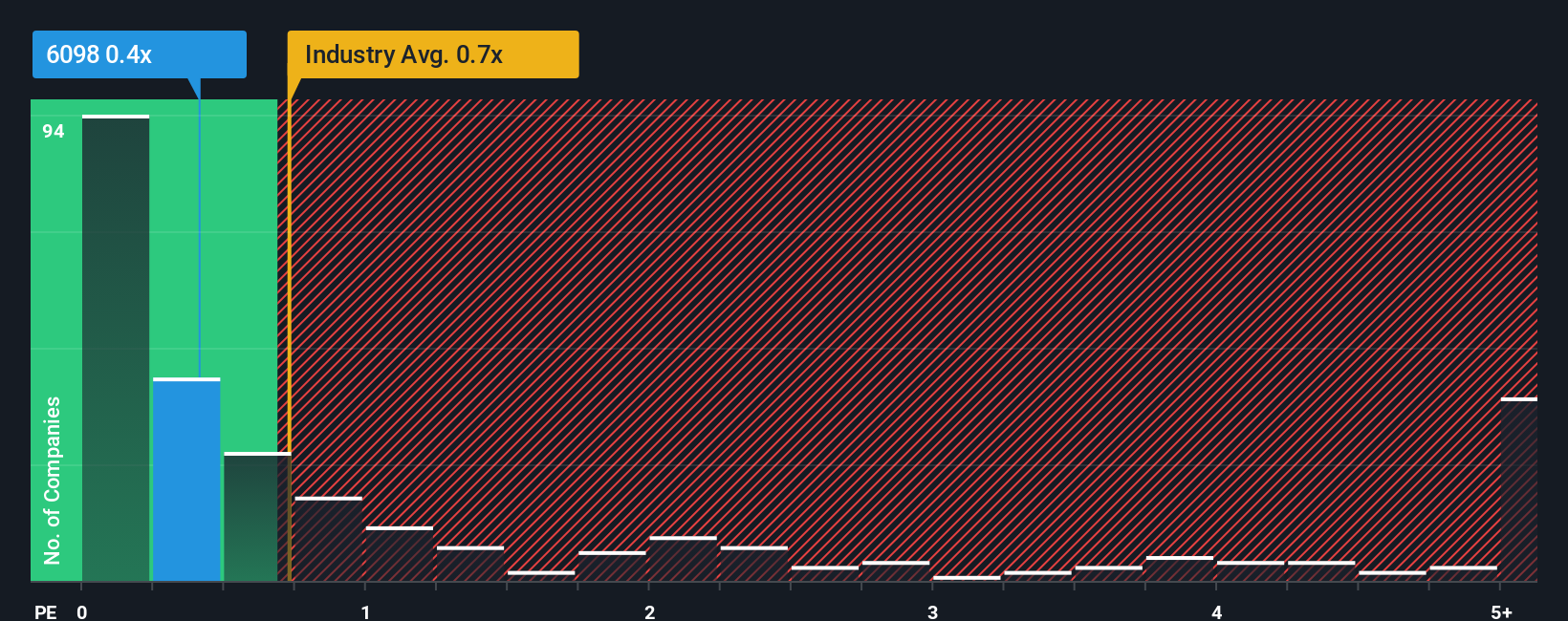

It’s not a stretch to say that Country Garden Services Holdings Company Limited’s (HKG:6098) price-to-sales (or “P/S”) ratio of 0.4x right now seems quite “middle-of-the-road” for companies in the Real Estate industry in Hong Kong, where the median P/S ratio is around 0.7x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Trump has pledged to “unleash” American oil and gas and these 15 US stocks have developments that are poised to benefit.

Check out our latest analysis for Country Garden Services Holdings

SEHK:6098 Price to Sales Ratio vs Industry November 21st 2025 What Does Country Garden Services Holdings’ Recent Performance Look Like?

SEHK:6098 Price to Sales Ratio vs Industry November 21st 2025 What Does Country Garden Services Holdings’ Recent Performance Look Like?

Country Garden Services Holdings certainly has been doing a good job lately as it’s been growing revenue more than most other companies. One possibility is that the P/S ratio is moderate because investors think this strong revenue performance might be about to tail off. If you like the company, you’d be hoping this isn’t the case so that you could potentially pick up some stock while it’s not quite in favour.

If you’d like to see what analysts are forecasting going forward, you should check out our free report on Country Garden Services Holdings. How Is Country Garden Services Holdings’ Revenue Growth Trending?

There’s an inherent assumption that a company should be matching the industry for P/S ratios like Country Garden Services Holdings’ to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 7.5% last year. The latest three year period has also seen a 24% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 2.0% per year over the next three years. That’s shaping up to be similar to the 3.8% each year growth forecast for the broader industry.

With this in mind, it makes sense that Country Garden Services Holdings’ P/S is closely matching its industry peers. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Final Word

We’d say the price-to-sales ratio’s power isn’t primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our look at Country Garden Services Holdings’ revenue growth estimates show that its P/S is about what we expect, as both metrics follow closely with the industry averages. At this stage investors feel the potential for an improvement or deterioration in revenue isn’t great enough to push P/S in a higher or lower direction. Unless these conditions change, they will continue to support the share price at these levels.

Having said that, be aware Country Garden Services Holdings is showing 2 warning signs in our investment analysis, you should know about.

It’s important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Explore Now for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Comments are closed.