Losses Persist, Challenging Bullish Narratives on Premium Valuation")

Madison Square Garden Sports (MSGS) reduced its losses at an impressive rate of 43.8% per year over the past five years, but remains unprofitable and is expected to stay that way for at least the next three years. While revenue is forecast to grow at 4% annually, which is well behind the broader US market’s 10.3%, shares are trading at $214.39, a premium against both peer and industry averages. The Price-To-Sales ratio is at 5x compared to 2.5x and 1.6x for peers and the industry, respectively. These premium multiples, in the face of slow growth and continued losses, highlight that investors may be balancing moderate risk of ongoing unprofitability against the chance for sentiment-driven price appreciation.

See our full analysis for Madison Square Garden Sports.

Now, let’s compare these numbers to the most persistent narratives shaping MSGS’s story and see which ones hold up to the latest data.

See what the community is saying about Madison Square Garden Sports

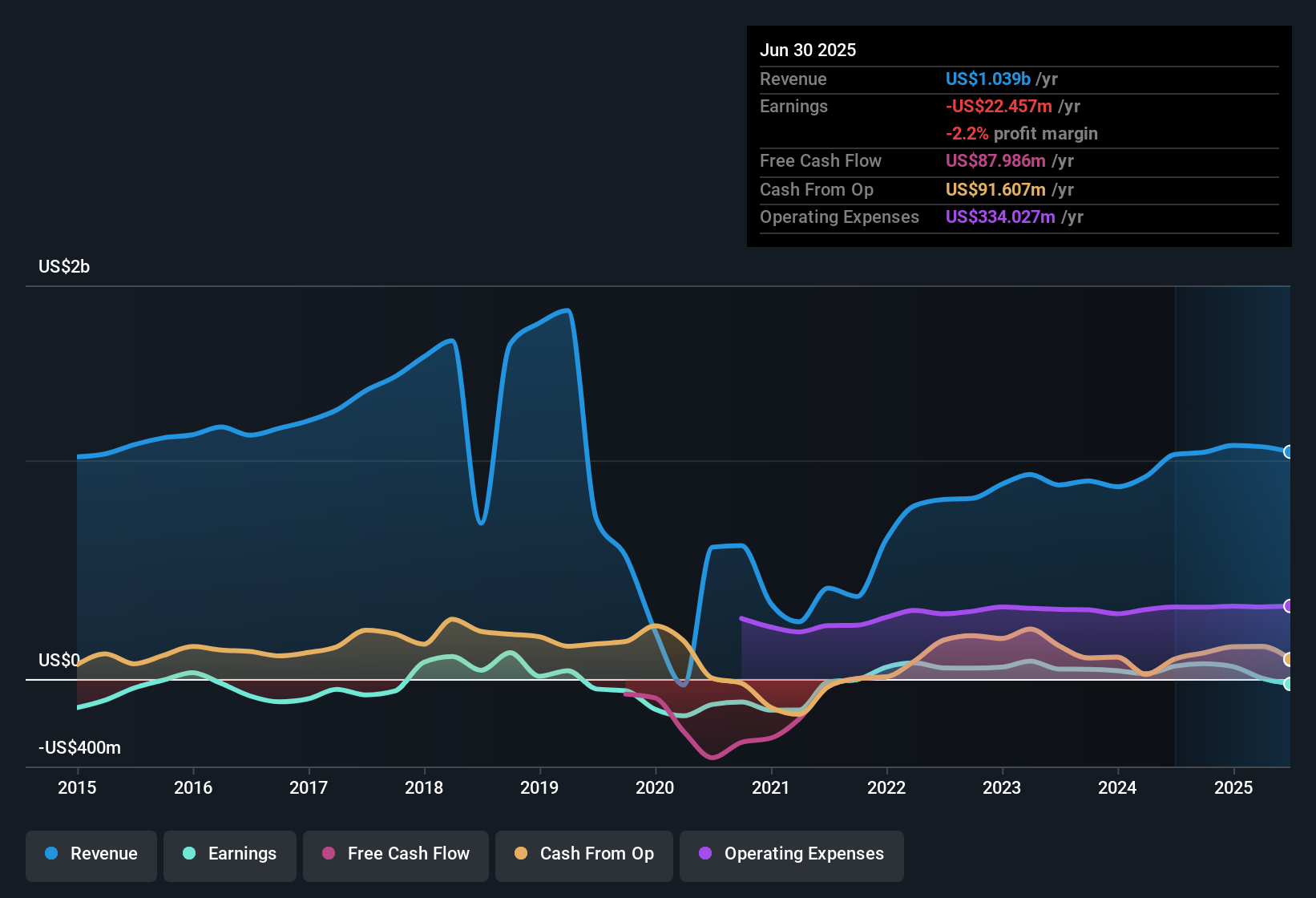

NYSE:MSGS Earnings & Revenue History as at Nov 2025 National Media Fees Set to Offset Local Revenue Slide The company’s ramp-up in high-value national media rights fees for the NBA, starting fiscal 2026, is forecast to offset reduced annual local media rights fees that recently fell by 28% for the Knicks and 18% for the Rangers. According to the analysts’ consensus view, the upcoming influx from national media rights is expected to greatly strengthen recurring revenue and improve margins. The loss of escalators and shorter contracts in local deals introduces a more volatile element, especially since only two teams drive the vast majority of earnings.

NYSE:MSGS Earnings & Revenue History as at Nov 2025 National Media Fees Set to Offset Local Revenue Slide The company’s ramp-up in high-value national media rights fees for the NBA, starting fiscal 2026, is forecast to offset reduced annual local media rights fees that recently fell by 28% for the Knicks and 18% for the Rangers. According to the analysts’ consensus view, the upcoming influx from national media rights is expected to greatly strengthen recurring revenue and improve margins. The loss of escalators and shorter contracts in local deals introduces a more volatile element, especially since only two teams drive the vast majority of earnings.

Analysts highlight that the additional national fees may provide an overall increase in recurring media revenue. They also underscore that reliance on just the Knicks and Rangers, along with shorter contract terms, makes MSG Sports especially sensitive to shifts in team performance and market cycles. Consensus also notes expanded international marketing partnerships are poised to boost sponsorships and global revenue streams, partially balancing the hit from declining local fees.

Consensus sees MSGS’s evolving media strategy as a double-edged sword, with increased national exposure but lingering risk tied to its concentrated asset base.

📊 Read the full Madison Square Garden Sports Consensus Narrative.

Event and Merchandise Revenue Highly Sensitive to Playoff Runs Merchandise and event-related revenues have declined year-over-year, with the company itself noting that both categories are “closely tied to special initiatives or deep playoff runs,” spotlighting significant earnings volatility tied to seasonal fan engagement. As the analysts’ consensus narrative explains, persistent demand for premium live sports and arena experiences will drive stable or accelerating event-related revenue, but actual growth depends on successful fan engagement strategies and strong team performance.

The consensus narrative calls out robust pricing power as evidenced by high ticket renewal rates. However, these gains are fragile without continued playoff participation or new in-arena offerings. Consensus flags that, absent consistent team success or new initiatives, both merchandise and event revenue could stagnate, capping top-line growth in future years. DCF Fair Value Gap and Premium Multiples Raise Valuation Questions Shares trade at $214.39, which is over 16 times higher than their DCF fair value of $13.00 and at a 5x Price-To-Sales ratio, significantly higher than peer (2.5x) and industry (1.6x) averages. The current price is also about 19% below the consensus analyst target of $263.67. The analysts’ consensus view points to a disconnect: current valuation implies investors must expect a profit margin swing from -2.2% to the 9.4% industry average over three years, and be comfortable with a potentially unsustainable PE of 80.7x on 2028 earnings.

Consensus puts the burden on improved earnings: to meet analyst targets, earnings must jump from -$22.5 million to $102.9 million by September 2028, an aggressive turnaround versus past trends and current unprofitability. Despite strong analyst price targets, the valuation is difficult to justify without substantial progress on both revenue growth and margin improvement well above MSGS’s recent track record. Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Madison Square Garden Sports on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

Have a fresh take on the figures? Share your own perspective and shape your narrative. In just a few minutes, you can take the lead. Do it your way

A great starting point for your Madison Square Garden Sports research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Madison Square Garden Sports’s high valuation and volatile earnings outlook expose investors to significant uncertainty around achieving stable growth and consistent profitability.

If you want steadier returns and reliable expansion, let our stable growth stocks screener (2103 results) guide you straight to companies delivering consistently strong earnings and revenue through all market cycles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Comments are closed.