Valuation After Strong Second Quarter Earnings")

Madison Square Garden Entertainment (MSGE) just posted second quarter results that caught investor attention, reporting revenue of US$459.94 million and net income of US$92.72 million, along with higher earnings per share from continuing operations.

See our latest analysis for Madison Square Garden Entertainment.

The latest earnings release and the extended Infosys partnership come on top of a strong run in the shares, with a 90 day share price return of 38.42% and a 1 year total shareholder return of 65.06%. This suggests momentum has been building around Madison Square Garden Entertainment at a last close of US$62.51.

If this kind of move has you looking for other ideas in entertainment and related themes, it could be worth checking out our screener of 23 top founder-led companies as a way to surface fresh names to research next.

With earnings growth, a completed buyback and a share price that has already moved sharply higher, the key question now is whether Madison Square Garden Entertainment still trades at a discount or if the market is already pricing in future growth.

Most Popular Narrative: 9% Undervalued

At a last close of $62.51 against a most followed fair value estimate of $68.71, the current price sits below where that narrative comes out. The gap rests on some fairly punchy assumptions about what these venues can earn over time.

Improved utilization and a strong event pipeline at key venues including the prospect of new multi date residencies at the Garden and sustained efficiency in theater bookings are set to unlock latent capacity and lift earnings consistency, supporting both free cash flow generation and potential for future buybacks.

Read the complete narrative.

Curious what has to go right for that valuation to hold up? Revenue growth, rising margins and a lower future P/E all sit at the core. The full narrative spells out how those pieces fit together, and what kind of earnings power that implies by the end of the forecast period.

Result: Fair Value of $68.71 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are still real pressure points to watch, particularly the heavy reliance on a few key venues and the sensitivity to discretionary consumer spending.

Find out about the key risks to this Madison Square Garden Entertainment narrative.

Another Angle On Valuation

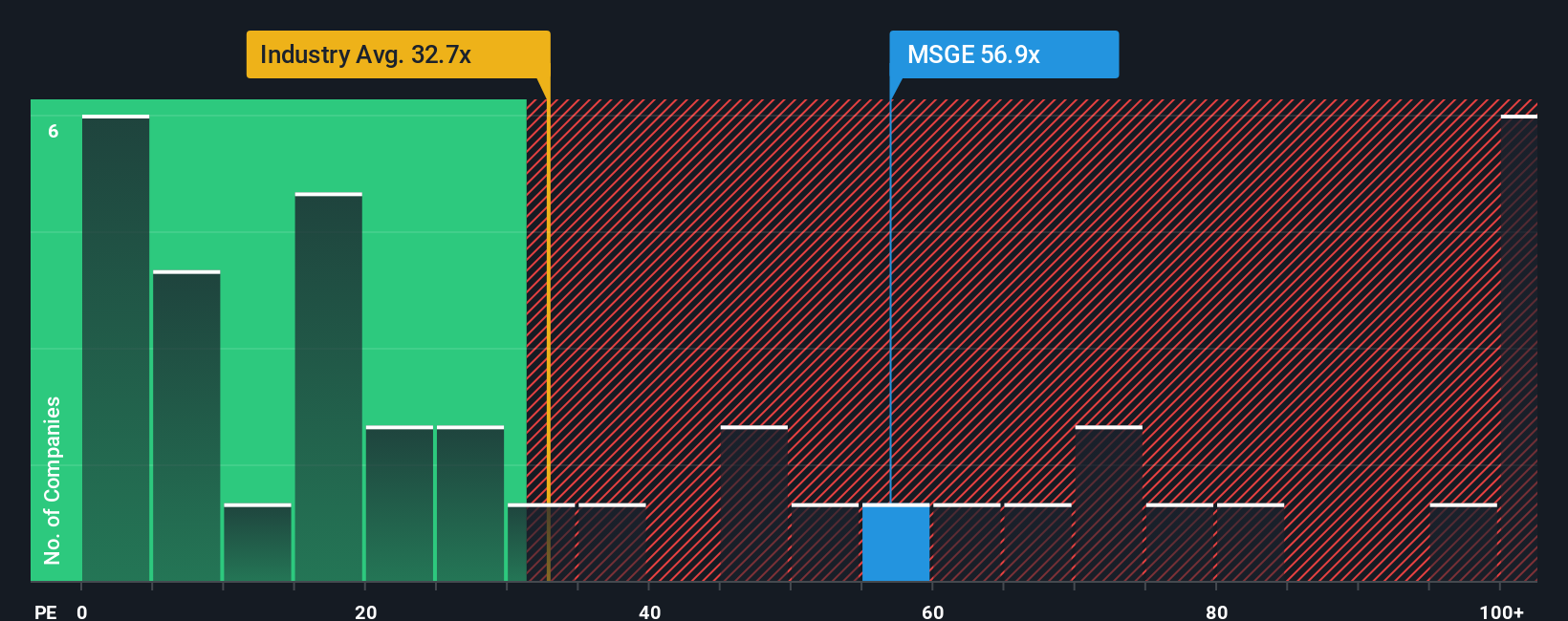

The fair value story so far leans on future cash flows and earnings power, but the current P/E ratio of 56.9x paints a different picture. It sits above the estimated fair ratio of 26.9x and above the US Entertainment industry at 32.7x, even though it is slightly below the 60.4x peer average.

That mix of richer pricing than the industry, a premium to the fair ratio the market could move toward, and only a small discount to peers raises a simple question for you: does this look more like valuation risk building up, or a premium the business can justify over time?

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:MSGE P/E Ratio as at Feb 2026 Build Your Own Madison Square Garden Entertainment Narrative

NYSE:MSGE P/E Ratio as at Feb 2026 Build Your Own Madison Square Garden Entertainment Narrative

If you see the numbers differently or prefer to stress test the assumptions yourself, you can build a custom view of the story in minutes: Do it your way.

A great starting point for your Madison Square Garden Entertainment research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If MSG Entertainment has sharpened your focus, do not stop here. Use the same structured tools to spot other opportunities before they appear on everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Comments are closed.