Valuation Following Goldman Sachs’ Bullish Endorsement")

Goldman Sachs just added Madison Square Garden Entertainment (MSGE) to its US Conviction List after observing a boost in concert bookings and an increase in Christmas Spectacular shows scheduled. The endorsement suggests higher revenue growth expectations.

See our latest analysis for Madison Square Garden Entertainment.

Thanks to strong demand for live shows and a growing slate of events, Madison Square Garden Entertainment’s momentum appears to be building. The stock’s 1-year total shareholder return is 0.09%, and its steady 30-day and 90-day share price gains suggest that optimism is on the rise after a period of slower growth.

If upbeat concert trends have you thinking broader, now could be the perfect time to discover fast growing stocks with high insider ownership.

But with shares currently trading just under their analyst target price and strong demand fueling optimism, investors must wonder if this is a hidden value opportunity or if the market has already priced in all the expected upside.

Most Popular Narrative: Fairly Valued

At $45.58 per share, Madison Square Garden Entertainment trades just above the most widely followed narrative’s fair value estimate. The stock’s price is almost exactly in line with the consensus, reflecting a market largely aligned with earnings expectations. Here’s what’s driving that stance:

Ongoing investments in premium hospitality and suite renovations, coupled with rising urban affluence and focus on upgrading the guest experience, are expected to further boost ancillary and high-margin revenue streams, improving overall profitability.

Read the complete narrative.

Want to unpack the strategy that’s got everyone watching? The narrative relies on a surprising combination of premium experiences, pricing power, and an ambitious profit transformation. What precise trends are shaping this valuation? Find out in the full breakdown. There is more beneath the surface than you might expect.

Result: Fair Value of $44.88 (ABOUT RIGHT)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, setbacks such as fewer marquee events or a slowdown in discretionary consumer spending could quickly challenge this balanced outlook for Madison Square Garden Entertainment.

Find out about the key risks to this Madison Square Garden Entertainment narrative.

Another Perspective: Discounted Cash Flow Model

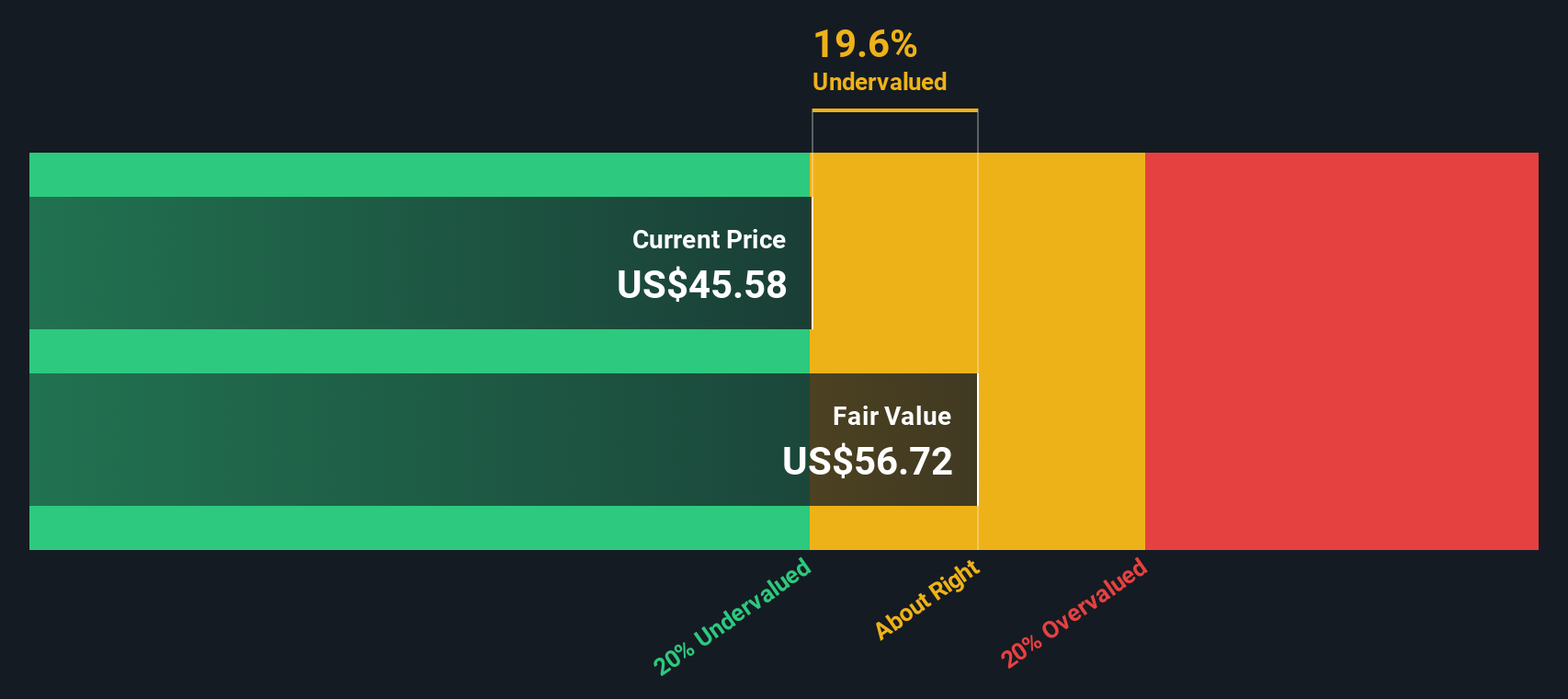

While analysts peg Madison Square Garden Entertainment’s fair value near its current price, our DCF model points to a different potential outlook. According to this method, shares are trading at nearly 20% below their estimated fair value, suggesting there may be untapped upside that consensus isn’t fully factoring in. Which number tells the deeper truth for investors?

Look into how the SWS DCF model arrives at its fair value.

MSGE Discounted Cash Flow as at Oct 2025

MSGE Discounted Cash Flow as at Oct 2025

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Madison Square Garden Entertainment for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Build Your Own Madison Square Garden Entertainment Narrative

If you have your own take or want to dig into the details yourself, it only takes a few minutes to craft your own view. Do it your way

A great starting point for your Madison Square Garden Entertainment research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Why settle for the usual picks when your next winning stock could be just a click away? Sharpen your portfolio with powerful trends and untapped sectors using Simply Wall Street’s screener tools before others catch on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Comments are closed.